DeFi doesn't have a liquidity problem. It has four hundred liquidity problems, one per chain, and they’re all the same problem repeated. We spent two years proving a model that solves it. Now we're scaling it everywhere.

tldr;

- Clovis is a cross-chain clearing and settlement layer where one deposit earns across lending, trading, and bridging simultaneously

- Built on the foundation of Yei Finance: $400M ATH TVL, $7.3M protocol revenue, 275k+ wallets, integrated into Binance Wallet

- Testnet now live

What two years taught us

We started on Sei with a simple thesis: DeFi users shouldn't have to choose between lending, trading, and bridging. Each primitive generates yield. Why force users to pick one?

So we built all three.

Yei Finance grew into the largest lending protocol on Sei, reaching $400M in TVL at its peak. YeiSwap processed over $535M in cumulative trading volume. YeiBridge moved $147M in cross-chain transfers and became the primary onramp for the Sei ecosystem. Revenue hit $7.3M. Binance Wallet integrated us natively, where their users could deposit into Yei without leaving the wallet.

The numbers proved that the primitives worked. But building them taught us something the numbers didn't show.

Each product, lending, DEX, and bridge, had its own pool of capital. Lending deposits sat idle when utilization was low. Bridge liquidity buffers waited between transfers. DEX positions only earned during trades. Three pools of capital, all serving the same users, none talking to each other.

That wasn't a Yei problem. It was the industry's design pattern. Every chain runs the same playbook: deploy a lending market, deploy a DEX, deploy a bridge. Each starts from zero. Each holds its own capital. Each operates as if the others don't exist.

We kept seeing the same inefficiency repeated not across competitors, but within our own stack. The bottleneck wasn't the primitives. It was their isolation.

The problem nobody frames correctly

Everyone in DeFi talks about fragmentation. But the conversation usually stops at "liquidity is spread across too many chains." That's a symptom. The structural problem runs deeper.

Look at the largest lending protocol in DeFi. Aave holds billions in TVL, but the vast majority sits on Ethereum. The rest is split across more than a dozen other chains. Same protocol, same smart contracts, zero shared liquidity between deployments. A deposit on Arbitrum does nothing for rates on Base.

The rate disparity tells the story clearly. USDC has earned as low as 1.08% APR on one Aave deployment and 8.06% on another — a 7x spread on the same asset, in the same protocol. Even in quieter markets, the gap persists: our data below shows spreads of up to 3.5x across major protocols today.

Rate differential, the average spread between an asset's rates across all chain deployments, is the clearest metric for measuring how fragmented DeFi liquidity really is. A high rate differential means capital is siloed. A low one means it's flowing freely. Right now, the differential across major protocols is massive, and that's the problem we’re solving.

The deeper issue: primitives that exist on every chain can't compose across chains. A deposit into a lending market can't simultaneously earn trading fees on a DEX. A bridge buffer holds capital that sits idle between transfers. Research suggests that the majority of cross-chain volume could be netted, meaning the industry physically moves far more capital between chains than final settlement requires.

Capital is everywhere. It's just not connected.

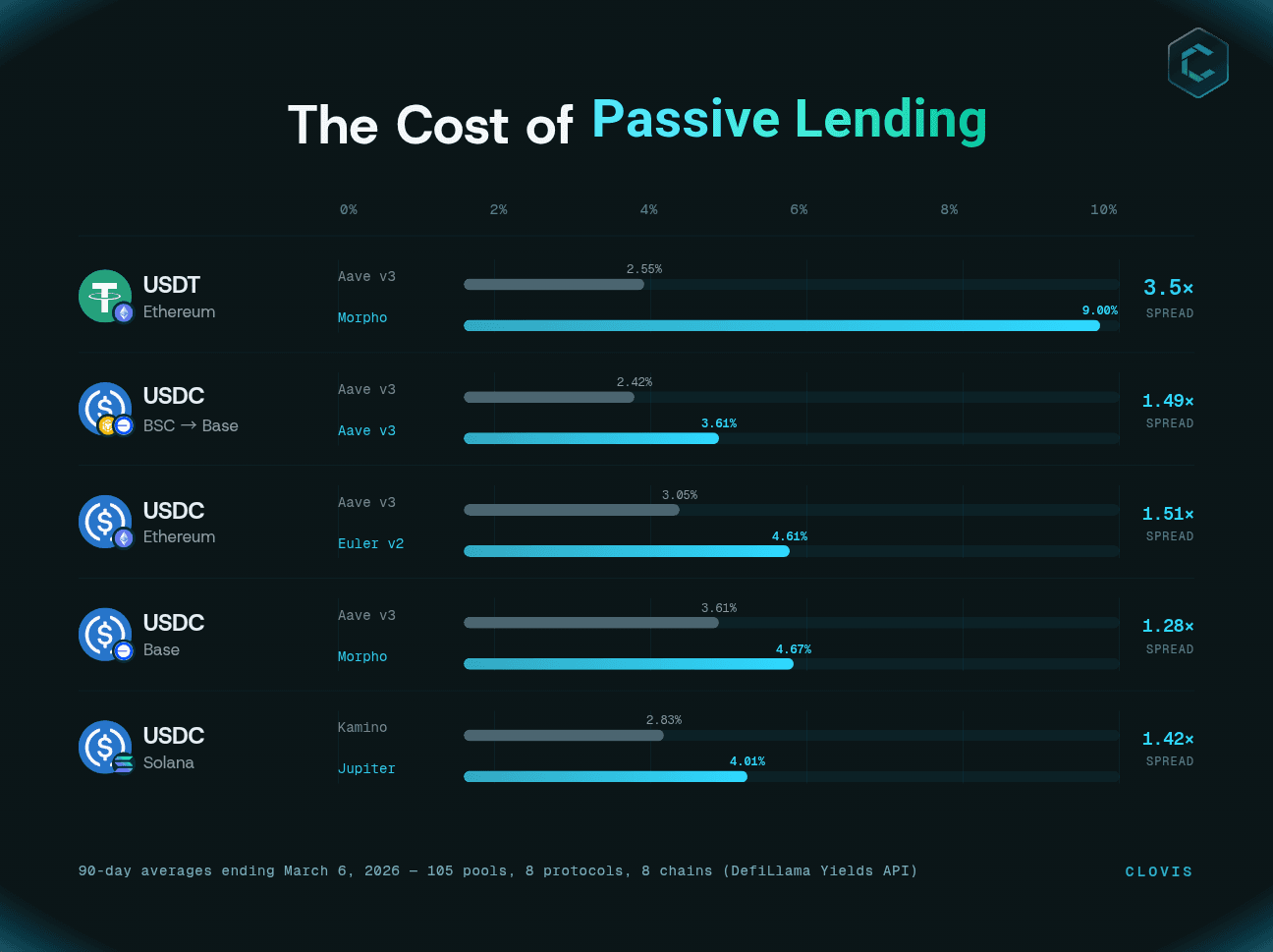

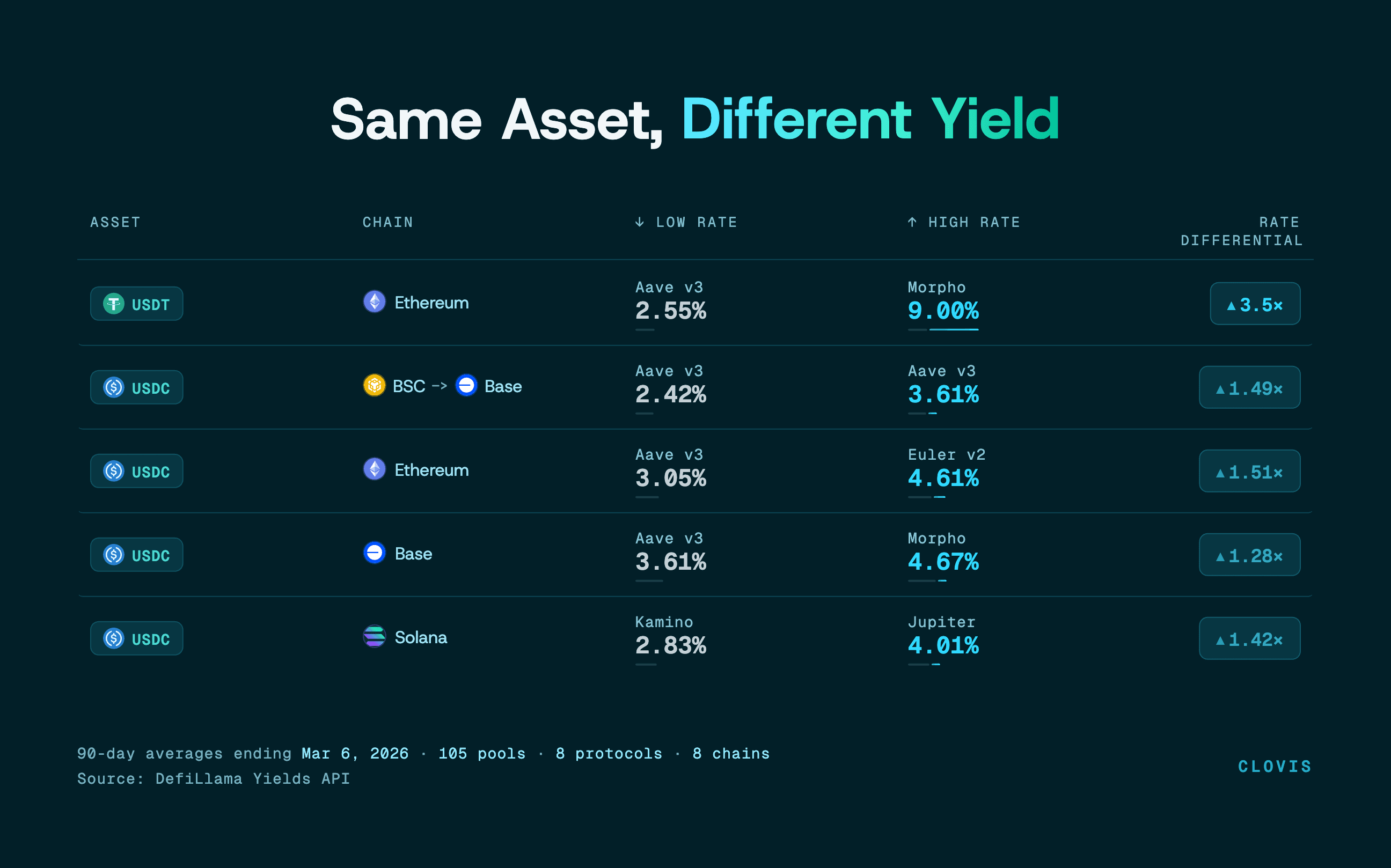

Rate Differentials: The Hidden Cost of Passive Lending

Data sources: 90-day averages ending March 6, 2026 - 105 pools, 8 protocols, 8 chains (Source: DefiLlama Yields API)

DeFi lending rates are fragmented by design. The same asset, on the same chain, earns wildly different yields depending on where you deposit. Across chains, the gap widens further.

$1.35B sitting at below-average rates. Aave v3 holds $1.35B in USDC on Ethereum at 3.05% APY. On the same chain, Morpho vaults pay 3.65-3.71% at $100M+ scale - a 20% premium worth ~$8.8M/year on that capital.

Same protocol, different chain, different yield. Aave v3 USDC ranges from 3.61% on Base to 2.42% on BSC - a 1.49x spread for identical risk.

At scale, the spread is real. Morpho's Sky Money USDT vault earns 9.00% ($89M TVL) while Aave USDT on the same chain pays 2.55% ($1.64B TVL) - a 3.5x multiplier.

This is a structural inefficiency. Every chain, protocol, and vault is an isolated liquidity silo. Every isolated pool is a missed opportunity for the capital sitting in it.

What if the primitives shared a backbone?

The insight that came from building Yei was architectural. Lending, trading, and bridging all need the same things: asset accounting, rate calculation, and risk math. But every deployment rebuilds that logic from scratch. What if you separated those two functions: the accounting (what assets exist, what rates should be) from the settlement (where users actually touch their tokens)?

That separation is what Clovis does.

A high-performance clearing layer handles the global logic: balances, utilization curves, interest rates, price computation. Lightweight vaults on every connected chain handle local custody and user-facing settlement. The clearing layer is the brain. The vaults are the hands.

The result is something that didn't exist before in DeFi: A single deposit simultaneously earns lending interest, trading fees when used as LP collateral, and bridge fees when idle capital settles transfers. Three yield streams from one deposit. The same USDC deposit rate whether you're on Ethereum, Arbitrum, or Base.

When Clovis is live, rate differential across chains should converge toward zero. Same asset, same rate, regardless of where you deposited. That's what happens when capital flows freely across a unified backbone instead of sitting in isolated pools.

This surfaces as four capabilities. Clovis Market handles lending and borrowing with universal rates across chains. Clovis Exchange pairs trading with lending deposits so LPs earn swap fees on top of lending yield. Clovis Transport settles bridge transfers instantly from local liquidity buffers instead of waiting for cross-chain messages. Clovis Vaults deploy idle capital sitting in those buffers into external yield opportunities matched to risk profiles.

None of these are standalone products. They're surfaces on the same liquidity.

What this changes

For new chains, this eliminates what we call the cold-start trap. Today, a new L1 or L2 has to bootstrap lending, trading, and bridging from zero: attract LPs, seed pools, incentivize deposits. With Clovis, they integrate once and get all three primitives with shared liquidity from day one. No separate bootstrapping. No starting from scratch.

For existing protocols and local markets, Clovis creates a new dynamic. Universal rates across chains produce natural arbitrage with local lending and trading rates. That arbitrage deepens liquidity for everyone. We complement local DeFi rather than replacing it.

For users, the "which chain should I deposit on?" question disappears. Deposit on any chain, access every yield source. The same rate, the same liquidity depth, regardless of where you are.

The capital efficiency gains compound. Netting reduces physical bridge transactions by roughly 70%. Stacking lending, trading, and bridging yield means every deposited dollar generates returns from multiple sources simultaneously. Capital works harder because the system is designed to let it.

What comes next

Clovis testnet is live. It demonstrates the core model in action: cross-chain deposits, unified interest rates, and the clearing-and-settlement architecture handling real transactions across multiple chains. After testnet, the path leads to mainnet and expanded chain support.

We'll share more as we get closer. For now, follow on Twitter to stay in the loop.

DeFi has 400 versions of the same three primitives, all isolated, all starting from zero. We spent two years proving that lending, trading, and bridging work better when they share a backbone. Now we're connecting every chain to it.

Deposit once. Earn everywhere.